Note

Go to the end to download the full example code

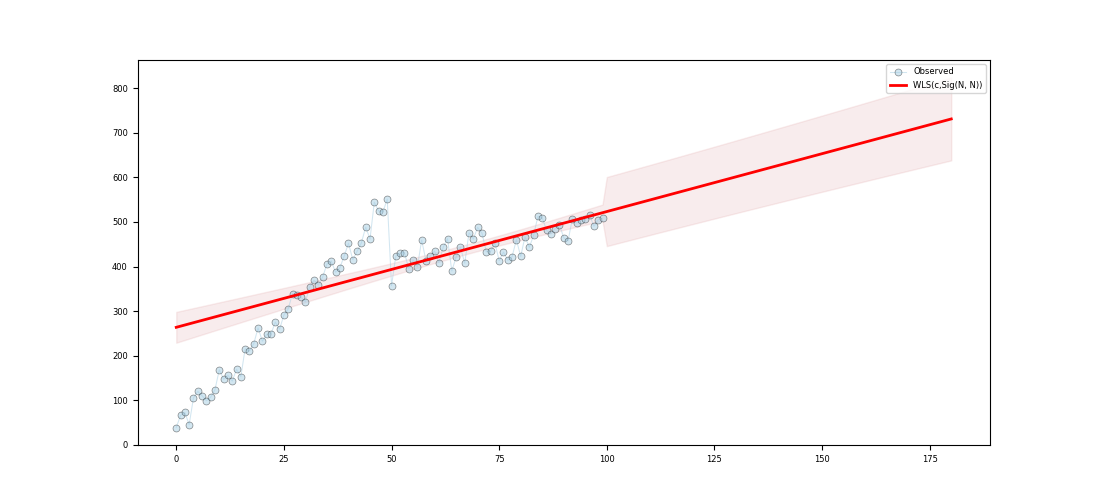

SART - Trend as slope of WLS

c:\users\kelda\desktop\repositories\virtualenvs\venv-py391-pyamr\lib\site-packages\statsmodels\regression\linear_model.py:807: RuntimeWarning:

divide by zero encountered in log

Series:

wls-rsquared 0.5402

wls-rsquared_adj 0.5355

wls-fvalue 115.1527

wls-fprob 0.0

wls-aic inf

wls-bic inf

wls-llf -inf

wls-mse_model 165533.2802

wls-mse_resid 1437.5111

wls-mse_total 3095.0441

wls-const_coef 263.575

wls-const_std 17.4154

wls-const_tvalue 15.1346

wls-const_tprob 0.0

wls-const_cil 229.0148

wls-const_ciu 298.1352

wls-x1_coef 2.5975

wls-x1_std 0.2421

wls-x1_tvalue 10.7309

wls-x1_tprob 0.0

wls-x1_cil 2.1171

wls-x1_ciu 3.0778

wls-s_dw 0.546

wls-s_jb_value 14.895

wls-s_jb_prob 0.0006

wls-s_skew 0.697

wls-s_kurtosis 4.278

wls-s_omnibus_value 12.662

wls-s_omnibus_prob 0.002

wls-m_dw 0.1707

wls-m_jb_value 4.7339

wls-m_jb_prob 0.0938

wls-m_skew -0.5009

wls-m_kurtosis 3.364

wls-m_nm_value 5.3656

wls-m_nm_prob 0.0684

wls-m_ks_value 0.5809

wls-m_ks_prob 0.0

wls-m_shp_value 0.9455

wls-m_shp_prob 0.0004

wls-m_ad_value 2.4183

wls-m_ad_nnorm False

wls-missing raise

wls-exog [[1.0, 0.0...

wls-endog [38.780154...

wls-trend c

wls-weights [0.0328805...

wls-W <pyamr.met...

wls-model <statsmode...

wls-id WLS(c,Sig(...

dtype: object

Regression line:

[263.58 266.17 268.77 271.37 273.96 276.56 279.16 281.76 284.35 286.95]

Summary:

WLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.540

Model: WLS Adj. R-squared: 0.536

Method: Least Squares F-statistic: 115.2

Date: Thu, 15 Jun 2023 Prob (F-statistic): 3.16e-18

Time: 18:17:11 Log-Likelihood: -inf

No. Observations: 100 AIC: inf

Df Residuals: 98 BIC: inf

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 263.5750 17.415 15.135 0.000 229.015 298.135

x1 2.5975 0.242 10.731 0.000 2.117 3.078

==============================================================================

Omnibus: 12.662 Durbin-Watson: 0.546

Prob(Omnibus): 0.002 Jarque-Bera (JB): 14.895

Skew: 0.697 Prob(JB): 0.000583

Kurtosis: 4.278 Cond. No. 231.

Normal (N): 5.366 Prob(N): 0.068

==============================================================================

14 # Import class.

15 import sys

16 import numpy as np

17 import pandas as pd

18 import matplotlib as mpl

19 import matplotlib.pyplot as plt

20 import statsmodels.api as sm

21 import statsmodels.robust.norms as norms

22

23 # import weights.

24 from pyamr.datasets.load import make_timeseries

25 from pyamr.core.regression.wls import WLSWrapper

26 from pyamr.metrics.weights import SigmoidA

27

28 # ----------------------------

29 # set basic configuration

30 # ----------------------------

31 # Matplotlib options

32 mpl.rc('legend', fontsize=6)

33 mpl.rc('xtick', labelsize=6)

34 mpl.rc('ytick', labelsize=6)

35

36 # Set pandas configuration.

37 pd.set_option('display.max_colwidth', 14)

38 pd.set_option('display.width', 150)

39 pd.set_option('display.precision', 4)

40

41 # ----------------------------

42 # create data

43 # ----------------------------

44 # Create timeseries data

45 x, y, f = make_timeseries()

46

47 # Create method to compute weights from frequencies

48 W = SigmoidA(r=200, g=0.5, offset=0.0, scale=1.0)

49

50 # Note that the function fit will call M.weights(weights) inside and will

51 # store the M converter in the instance. Therefore, the code executed is

52 # equivalent to <weights=M.weights(f)> with the only difference being that

53 # the weight converter is not saved.

54 wls = WLSWrapper(estimator=sm.WLS).fit( \

55 exog=x, endog=y, trend='c', weights=f,

56 W=W, missing='raise')

57

58 # Print series.

59 print("\nSeries:")

60 print(wls.as_series())

61

62 # Print regression line.

63 print("\nRegression line:")

64 print(wls.line(np.arange(10)))

65

66 # Print summary.

67 print("\nSummary:")

68 print(wls.as_summary())

69

70 # -----------------

71 # Save & Load

72 # -----------------

73 # File location

74 #fname = '../../examples/saved/wls-sample.pickle'

75

76 # Save

77 #wls.save(fname=fname)

78

79 # Load

80 #wls = WLSWrapper().load(fname=fname)

81

82 # -------------

83 # Example I

84 # -------------

85 # This example shows how to make predictions using the wrapper and how

86 # to plot the resultin data. In addition, it compares the intervales

87 # provided by get_prediction (confidence intervals) and the intervals

88 # provided by wls_prediction_std (prediction intervals).

89 #

90 # To Do: Implement methods to compute CI and PI (see regression).

91

92 # Variables.

93 start, end = None, 180

94

95 # Compute predictions (exogenous?). It returns a 2D array

96 # where the rows contain the time (t), the mean, the lower

97 # and upper confidence (or prediction?) interval.

98 preds = wls.get_prediction(start=start, end=end)

99

100

101 # Create figure

102 fig, ax = plt.subplots(1, 1, figsize=(11,5))

103

104 # Plotting confidence intervals

105 # -----------------------------

106 # Plot truth values.

107 ax.plot(x, y, color='#A6CEE3', alpha=0.5, marker='o',

108 markeredgecolor='k', markeredgewidth=0.5,

109 markersize=5, linewidth=0.75, label='Observed')

110

111 # Plot forecasted values.

112 ax.plot(preds[0,:], preds[1, :], color='#FF0000', alpha=1.00,

113 linewidth=2.0, label=wls._identifier(short=True))

114

115 # Plot the confidence intervals.

116 ax.fill_between(preds[0, :], preds[2, :],

117 preds[3, :],

118 color='r',

119 alpha=0.1)

120

121 # Legend

122 plt.legend()

123

124 # Show

125 plt.show()

Total running time of the script: ( 0 minutes 0.108 seconds)