Note

Go to the end to download the full example code

WLS - Basic

c:\users\kelda\desktop\repositories\virtualenvs\venv-py391-pyamr\lib\site-packages\statsmodels\regression\linear_model.py:807: RuntimeWarning:

divide by zero encountered in log

Series:

wls-rsquared 0.4773

wls-rsquared_adj 0.472

wls-fvalue 89.4894

wls-fprob 0.0

wls-aic inf

wls-bic inf

wls-llf -inf

wls-mse_model 137903.9406

wls-mse_resid 1541.008

wls-mse_total 2918.4114

wls-const_coef 275.6131

wls-const_std 18.2135

wls-const_tvalue 15.1324

wls-const_tprob 0.0

wls-const_cil 239.469

wls-const_ciu 311.7571

wls-x1_coef 2.405

wls-x1_std 0.2542

wls-x1_tvalue 9.4599

wls-x1_tprob 0.0

wls-x1_cil 1.9005

wls-x1_ciu 2.9095

wls-s_dw 0.488

wls-s_jb_value 7.949

wls-s_jb_prob 0.0188

wls-s_skew 0.566

wls-s_kurtosis 3.791

wls-s_omnibus_value 8.126

wls-s_omnibus_prob 0.017

wls-m_dw 0.1295

wls-m_jb_value 6.1737

wls-m_jb_prob 0.0456

wls-m_skew -0.5865

wls-m_kurtosis 3.325

wls-m_nm_value 6.6625

wls-m_nm_prob 0.0357

wls-m_ks_value 0.5736

wls-m_ks_prob 0.0

wls-m_shp_value 0.9415

wls-m_shp_prob 0.0002

wls-m_ad_value 2.4991

wls-m_ad_nnorm False

wls-missing raise

wls-exog [[1.0, 0.0...

wls-endog [41.719565...

wls-trend c

wls-weights [0.0435648...

wls-W <pyamr.met...

wls-model <statsmode...

wls-id WLS(c,Sig(...

dtype: object

Regression line:

[275.61 278.02 280.42 282.83 285.23 287.64 290.04 292.45 294.85 297.26]

Summary:

WLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.477

Model: WLS Adj. R-squared: 0.472

Method: Least Squares F-statistic: 89.49

Date: Thu, 15 Jun 2023 Prob (F-statistic): 1.80e-15

Time: 18:19:13 Log-Likelihood: -inf

No. Observations: 100 AIC: inf

Df Residuals: 98 BIC: inf

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 275.6131 18.213 15.132 0.000 239.469 311.757

x1 2.4050 0.254 9.460 0.000 1.900 2.910

==============================================================================

Omnibus: 8.126 Durbin-Watson: 0.488

Prob(Omnibus): 0.017 Jarque-Bera (JB): 7.949

Skew: 0.566 Prob(JB): 0.0188

Kurtosis: 3.791 Cond. No. 234.

Normal (N): 6.662 Prob(N): 0.036

==============================================================================

6 # Import class.

7 import sys

8 import numpy as np

9 import pandas as pd

10 import matplotlib as mpl

11 import matplotlib.pyplot as plt

12 import statsmodels.api as sm

13 import statsmodels.robust.norms as norms

14

15 # import weights.

16 from pyamr.datasets.load import make_timeseries

17 from pyamr.core.regression.wls import WLSWrapper

18 from pyamr.metrics.weights import SigmoidA

19

20 # ----------------------------

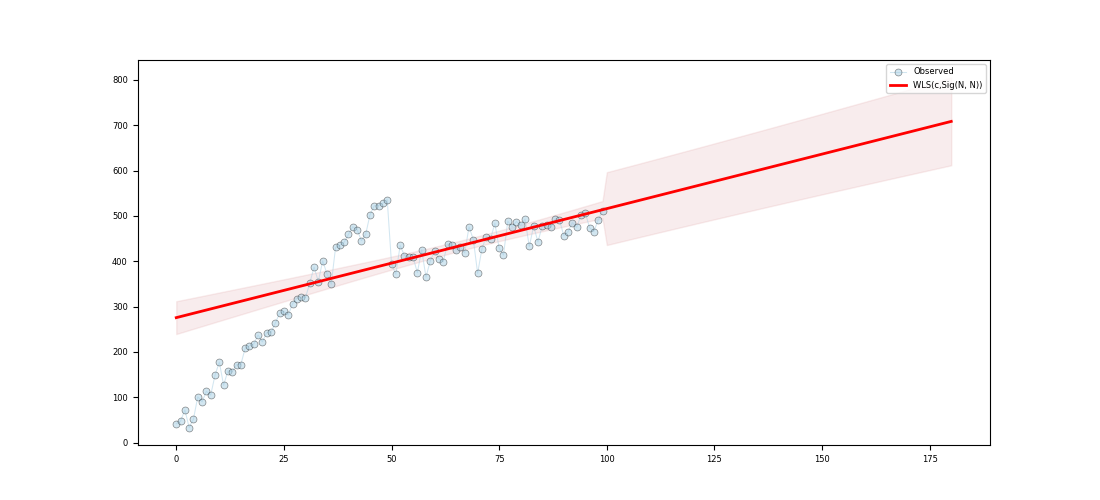

21 # set basic configuration

22 # ----------------------------

23 # Matplotlib options

24 mpl.rc('legend', fontsize=6)

25 mpl.rc('xtick', labelsize=6)

26 mpl.rc('ytick', labelsize=6)

27

28 # Set pandas configuration.

29 pd.set_option('display.max_colwidth', 14)

30 pd.set_option('display.width', 150)

31 pd.set_option('display.precision', 4)

32

33 # ----------------------------

34 # create data

35 # ----------------------------

36 # Create timeseries data

37 x, y, f = make_timeseries()

38

39 # Create method to compute weights from frequencies

40 W = SigmoidA(r=200, g=0.5, offset=0.0, scale=1.0)

41

42 # Note that the function fit will call M.weights(weights) inside and will

43 # store the M converter in the instance. Therefore, the code execute is

44 # equivalent to <weights=M.weights(f)> with the only difference being that

45 # the weight converter is not saved.

46 wls = WLSWrapper(estimator=sm.WLS).fit( \

47 exog=x, endog=y, trend='c', weights=f,

48 W=W, missing='raise')

49

50 # Print series.

51 print("\nSeries:")

52 print(wls.as_series())

53

54 # Print regression line.

55 print("\nRegression line:")

56 print(wls.line(np.arange(10)))

57

58 # Print summary.

59 print("\nSummary:")

60 print(wls.as_summary())

61

62 # -----------------

63 # Save & Load

64 # -----------------

65 # File location

66 #fname = '../../examples/saved/wls-sample.pickle'

67

68 # Save

69 #wls.save(fname=fname)

70

71 # Load

72 #wls = WLSWrapper().load(fname=fname)

73

74 # -------------

75 # Example I

76 # -------------

77 # This example shows how to make predictions using the wrapper and how

78 # to plot the resultin data. In addition, it compares the intervales

79 # provided by get_prediction (confidence intervals) and the intervals

80 # provided by wls_prediction_std (prediction intervals).

81 #

82 # To Do: Implement methods to compute CI and PI (see regression).

83

84 # Variables.

85 start, end = None, 180

86

87 # Compute predictions (exogenous?). It returns a 2D array

88 # where the rows contain the time (t), the mean, the lower

89 # and upper confidence (or prediction?) interval.

90 preds = wls.get_prediction(start=start, end=end)

91

92

93 # Create figure

94 fig, ax = plt.subplots(1, 1, figsize=(11,5))

95

96 # Plotting confidence intervals

97 # -----------------------------

98 # Plot truth values.

99 ax.plot(x, y, color='#A6CEE3', alpha=0.5, marker='o',

100 markeredgecolor='k', markeredgewidth=0.5,

101 markersize=5, linewidth=0.75, label='Observed')

102

103 # Plot forecasted values.

104 ax.plot(preds[0,:], preds[1, :], color='#FF0000', alpha=1.00,

105 linewidth=2.0, label=wls._identifier(short=True))

106

107 # Plot the confidence intervals.

108 ax.fill_between(preds[0, :], preds[2, :],

109 preds[3, :],

110 color='r',

111 alpha=0.1)

112

113 # Legend

114 plt.legend()

115

116 # Show

117 plt.show()

Total running time of the script: ( 0 minutes 0.114 seconds)