pyamr.core.stats.stationarity

Classes

- class pyamr.core.stats.stationarity.StationarityWrapper(estimator=None, evaluate=True)[source]

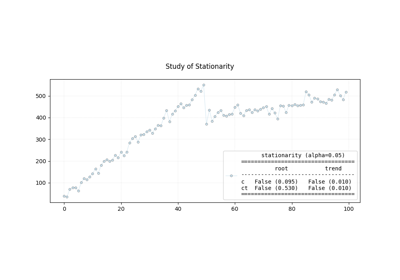

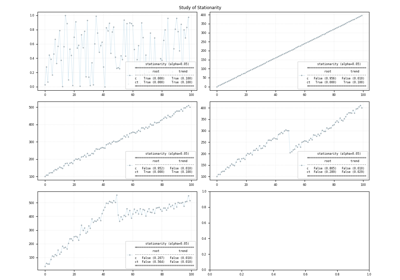

In time series analysis, “stationarity” refers to a key assumption about the behavior of a time series over time. A stationary time series is one in which statistical properties, such as mean, variance, and autocorrelation, remain constant over time. Stationarity is an important concept because many time series analysis techniques rely on this assumption for their validity. There are different types of stationarity that can be observed in time series data.

The augmented Dickey–Fuller test or

ADFcan be used to determine the presence of a unit root. When the other roots of the characteristic function lie inside the unit circle the first difference of the process is stationary. Due to this property, these are also called difference-stationary processes. Since the absence of unit root is not a proof of non-stationarity, the Kwiatkowski–Phillips–Schmidt–Shin orKPSStest can be used to identify the existence of an underlying trend which can also be removed to obtain a stationary process. These are called trend-stationary processes. In both, unit-root and trend-stationary processes, the mean can be increasing or decreasing over time; however, in the presence of a shock, trend-stationary processes (blue) revert to this mean tendency in the long run (deterministic trend) while unit-root processes (green) have a permanent impact (stochastic trend). The significance level of the tests is usually set to 0.05.ADF

KPSS

Outcome

Note

Non-StationaryNon-StationaryNon-StationaryStationaryStationaryStationaryNon-StationaryStationaryTrend-StationaryCheck the de-trended series

StationaryNon-StationaryDifference-StationaryCheck the differenced series

Methods:

as_summary([alpha])This method creates the summary to display.

evaluate([alpha])This method initialises the series.

fit(x[, adf_kwargs, kpss_kwargs])This method studies the stationarity of a given time-series.

- fit(x, adf_kwargs={}, kpss_kwargs={}, **kwargs)[source]

This method studies the stationarity of a given time-series.

The parameters which can be passed to the adfuller and kpss methods are listed below:

adfuller_kwargs = {x, maxlag, regression, autolag, store, regresults}

kpss_kwargs = {x, regression, lags, store}

@see statsmodels.tsa.stattools.adfuller @see statsmodels.tsa.stattoosl.kpss

- Parameters:

x (array-like) – The time series

adf_kwargs (dict-like) – The parameters to pass to the adfuller function

kpss_kwargs (dict-like) – The parameters to apss to the kpss function

- Returns:

object

- Return type:

An StationarityWrapper objects.