Note

Go to the end to download the full example code

Step 03 - Time Series Analysis

In this tutorial example, we will delve into the fascinating field of time series analysis and explore how to compute and analyze time series data. Time series analysis involves studying data points collected over regular intervals of time, with the aim of understanding patterns, trends, and relationships that may exist within the data. By applying statistical techniques, we can uncover valuable insights and make predictions based on historical trends.

Throughout this example, we will explore various statistical metrics and tests to that are commonly used for time series analysis, empowering you to harness the power of time-dependent data and extract meaningful information from it. The special focus is stationarity, which is a common requirements for further application of time series analysis methods.

See below for a few resources.

Create time series (TS)

First lets create an artificial series. The series has been plotted ad the end of the tutorial.

36 # ----------------------------

37 # create data

38 # ----------------------------

39 # Import specific

40 from pyamr.datasets.load import make_timeseries

41

42 # Create timeseries data

43 x, y, f = make_timeseries()

Pearson correlation coefficient

It measures the linear correlation between two variables with a value within the range [-1,1]. Coefficient values of -1, 0 and 1 indicate total negative linear correlation, no linear correlation and total positive correlation respectively. In this study, the coefficient is used to assess whether or not there is a linear correlation between the number of observations (susceptibility test records) and the computed resistance index.

See also Correlation

58 # -------------------------------

59 # Pearson correlation coefficient

60 # -------------------------------

61 # Import pyAMR

62 from pyamr.core.stats.correlation import CorrelationWrapper

63

64 # Create object

65 correlation = CorrelationWrapper().fit(x1=y, x2=f)

66

67 # Print summary.

68 print("\n")

69 print(correlation.as_summary())

Correlation

==============================

Pearson: 0.784

Spearman: 0.790

Cross correlation: 5114836.774

==============================

Augmented Dickey-Fuller test

The Augmented Dickey-Fuller or ADF test can be used to test for a unit root

in a univariate process in the presence of serial correlation. The intuition behind

a unit root test is that it determines how strongly a time series is defined by a trend.

ADF tests the null hypothesis that a unit root is present in a time series sample.

The alternative hypothesis is different depending on which version of the test is used,

but is usually stationarity or trend-stationarity. The more negative the statistic, the

stronger the rejection of the hypothesis that there is a unit root at some level

of confidence.

H |

Hypothesis |

Stationarity |

|---|---|---|

H0 |

The series has a unit root |

|

H1 |

The series has no unit root |

|

See also ADFuller

97 # ----------------------------

98 # ADFuller

99 # ----------------------------

100 # Import statsmodels

101 from statsmodels.tsa.stattools import adfuller

102

103 # Import pyAMR

104 from pyamr.core.stats.adfuller import ADFWrapper

105

106 # Create wrapper

107 adf = ADFWrapper(adfuller).fit(x=y, regression='ct')

108

109 print("\n")

110 print(adf.as_summary())

adfuller test stationarity (ct)

=======================================

statistic: -2.128

pvalue: 0.53020

nlags: 1

nobs: 98

stationarity (α=0.05): non-stationary

=======================================

Kwiatkowski-Phillips-Schmidt-Shin test

The Kwiatkowski–Phillips–Schmidt–Shin or KPSS test is used to identify

whether a time series is stationary around a deterministic trend (thus

trend stationary) against the alternative of a unit root.

In the KPSS test, the absence of a unit root is not a proof of stationarity but, by design, of trend stationarity. This is an important distinction since it is possible for a time series to be non-stationary, have no unit root yet be trend-stationary.

In both, unit-root and trend-stationary processes, the mean can be increasing or decreasing over time; however, in the presence of a shock, trend-stationary processes revert to this mean tendency in the long run (deterministic trend) while unit-root processes have a permanent impact (stochastic trend).

H |

Hypothesis |

Stationarity |

|---|---|---|

H0 |

The series has no unit root |

|

H1 |

The series has a unit root |

|

144 # --------------------------------

145 # Kpss

146 # --------------------------------

147 # Used within StationarityWrapper!

Understanding stationarity in TS

In time series analysis, “stationarity” refers to a key assumption about the behavior of a time series over time. A stationary time series is one in which statistical properties, such as mean, variance, and autocorrelation, remain constant over time. Stationarity is an important concept because many time series analysis techniques rely on this assumption for their validity. There are different types of stationarity that can be observed in time series data. Let’s explore them:

Strict Stationarity: A time series is considered strictly stationary if the joint probability distribution of any set of its time points is invariant over time. This means that the statistical properties, such as mean, variance, and covariance, are constant across all time points.

Weak Stationarity: Weak stationarity, also known as second-order stationarity or covariance stationarity, is a less strict form of stationarity. A time series is considered weakly stationary if its mean and variance are constant over time, and the autocovariance between any two time points only depends on the time lag between them. In other words, the statistical properties of the time series do not change with time.

Trend Stationarity: Trend stationarity refers to a time series that exhibits a stable mean over time but may have a changing variance. This means that the data has a consistent trend component but the other statistical properties remain constant. In trend stationary series, the mean of the time series can be modeled by a constant or a linear trend.

Difference Stationarity: Difference stationarity, also known as integrated stationarity, occurs when differencing a non-stationary time series results in a stationary series. Differencing involves computing the differences between consecutive observations to remove trends or other non-stationary patterns. A differenced time series is said to be difference stationary if it exhibits weak stationarity after differencing.

Seasonal Stationarity: …

The augmented Dickey–Fuller test or ADF can be used to determine the presence of a unit root.

When the other roots of the characteristic function lie inside the unit circle the first

difference of the process is stationary. Due to this property, these are also called

difference-stationary processes. Since the absence of unit root is not a proof of non-stationarity,

the Kwiatkowski–Phillips–Schmidt–Shin or KPSS test can be used to identify the existence of an

underlying trend which can also be removed to obtain a stationary process. These are called

trend-stationary processes. In both, unit-root and trend-stationary processes, the mean can be

increasing or decreasing over time; however, in the presence of a shock, trend-stationary

processes (blue) revert to this mean tendency in the long run (deterministic trend) while unit-root

processes (green) have a permanent impact (stochastic trend). The significance level of the tests

is usually set to 0.05.

ADF |

KPSS |

Outcome |

Note |

|---|---|---|---|

|

|

|

|

|

|

|

|

|

|

|

Check the de-trended series |

|

|

|

Check the differenced-series |

See also Stationarity

216 # ----------------------------

217 # Stationarity

218 # ----------------------------

219 # Import generic

220 import matplotlib.pyplot as plt

221

222 # Import pyAMR

223 from pyamr.core.stats.stationarity import StationarityWrapper

224

225 # Define kwargs

226 adf_kwargs = {}

227 kpss_kwargs = {}

228

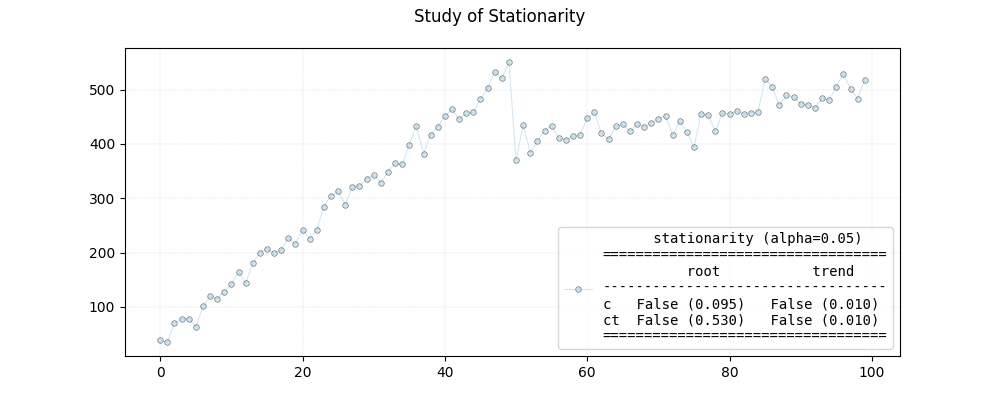

229 # Compute stationarity

230 stationarity = StationarityWrapper().fit(x=y,

231 adf_kwargs=adf_kwargs, kpss_kwargs=kpss_kwargs)

232

233 # Print summary.

234 print("\n")

235 print(stationarity.as_summary())

236

237

238 # ----------------

239 # plot

240 # ----------------

241 # Font type.

242 font = {

243 'family': 'monospace',

244 'weight': 'normal',

245 'size': 10,

246 }

247

248 # Create figure

249 fig, ax = plt.subplots(1, 1, figsize=(10, 4))

250

251 # Plot truth values.

252 ax.plot(y, color='#A6CEE3', alpha=0.5, marker='o',

253 markeredgecolor='k', markeredgewidth=0.5,

254 markersize=4, linewidth=0.75,

255 label=stationarity.as_summary())

256

257 # Format axes

258 ax.grid(color='gray', linestyle='--', linewidth=0.2, alpha=0.5)

259 ax.legend(prop=font, loc=4)

260

261 # Addd title

262 plt.suptitle("Study of Stationarity")

263

264 plt.show()

c:\users\kelda\desktop\repositories\github\pyamr\main\pyamr\core\stats\stationarity.py:187: InterpolationWarning:

The test statistic is outside of the range of p-values available in the

look-up table. The actual p-value is smaller than the p-value returned.

c:\users\kelda\desktop\repositories\github\pyamr\main\pyamr\core\stats\stationarity.py:188: InterpolationWarning:

The test statistic is outside of the range of p-values available in the

look-up table. The actual p-value is smaller than the p-value returned.

c:\users\kelda\desktop\repositories\github\pyamr\main\pyamr\core\stats\stationarity.py:189: InterpolationWarning:

The test statistic is outside of the range of p-values available in the

look-up table. The actual p-value is smaller than the p-value returned.

(3.2, 0.95, {'10%': 1.2888, '5%': 1.1412, '2.5%': 1.0243, '1%': 0.907})

stationarity (alpha=0.05)

==================================

root trend

----------------------------------

c False (0.095) False (0.010)

ct False (0.530) False (0.010)

==================================

Total running time of the script: ( 0 minutes 0.101 seconds)