Note

Go to the end to download the full example code

Using SARIMAX for seasonality

Approximate a function using Sesonal Autoregressive Integrated Moving Average (SARIMA)

Series:

sarimax-aic 765.3684

sarimax-bic 779.585

sarimax-hqic 771.064

sarimax-llf -376.6842

sarimax-intercept_coef 15.1175

...

sarimax-seasonal_order (1, 0, 1, 12)

sarimax-order (0, 1, 1)

sarimax-disp 0

sarimax-model <statsmode...

sarimax-id SARIMAX(0,...

Length: 73, dtype: object

Summary:

SARIMAX Results

==========================================================================================

Dep. Variable: y No. Observations: 80

Model: SARIMAX(0, 1, 1)x(1, 0, 1, 12) Log Likelihood -376.684

Date: Thu, 15 Jun 2023 AIC 765.368

Time: 18:15:49 BIC 779.585

Sample: 0 HQIC 771.064

- 80

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

intercept 15.1175 15.426 0.980 0.327 -15.117 45.352

drift -0.2044 0.236 -0.865 0.387 -0.667 0.258

ma.L1 -0.4005 0.097 -4.147 0.000 -0.590 -0.211

ar.S.L12 -0.2805 0.950 -0.295 0.768 -2.142 1.581

ma.S.L12 0.4495 0.873 0.515 0.606 -1.261 2.160

sigma2 804.6743 118.040 6.817 0.000 573.320 1036.028

==============================================================================

Ljung-Box(L1)(Q): 0.32 Jarque-Bera (JB): 14.26

Prob(Q): 0.57 Prob(JB): 0.00

Heteroskedasticity(H): 1.28 Skew: -0.79

Prob(H)(two-sided): 0.53 Kurtosis: 4.36

==============================================================================

Manual

------------------------------------------------------------------------------

Omnibus: 0.000 Durbin-Watson: 2.097

Normal (N): 11.607 Prob(N): 0.003

==============================================================================

Note that JB, P(JB), skew and kurtosis have different values.

Note that Prob(Q) tests no correlation of residuals.

8 # Import.

9 import sys

10 import warnings

11 import pandas as pd

12 import matplotlib as mpl

13 import matplotlib.pyplot as plt

14

15 # Import sarimax

16 from statsmodels.tsa.statespace.sarimax import SARIMAX

17

18 # import weights.

19 from pyamr.datasets.load import make_timeseries

20 from pyamr.core.regression.sarimax import SARIMAXWrapper

21

22 # Filter warnings

23 warnings.simplefilter(action='ignore', category=FutureWarning)

24

25 # ----------------------------

26 # set basic configuration

27 # ----------------------------

28 # Matplotlib options

29 mpl.rc('legend', fontsize=6)

30 mpl.rc('xtick', labelsize=6)

31 mpl.rc('ytick', labelsize=6)

32

33 # Set pandas configuration.

34 pd.set_option('display.max_colwidth', 14)

35 pd.set_option('display.width', 150)

36 pd.set_option('display.precision', 4)

37

38 # ----------------------------

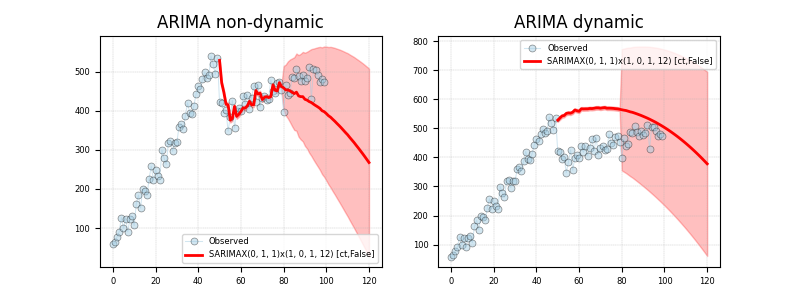

39 # create data

40 # ----------------------------

41 # Create timeseries data

42 x, y, f = make_timeseries()

43

44 # Create exogenous variable

45 exog = x

46

47 # ----------------------------

48 # fit the model

49 # ----------------------------

50 # Create specific sarimax model.

51 sarimax = SARIMAXWrapper(estimator=SARIMAX) \

52 .fit(endog=y[:80], exog=None, trend='ct',

53 seasonal_order=(1, 0, 1, 12), order=(0, 1, 1),

54 disp=0)

55

56 # Print series

57 print("\nSeries:")

58 print(sarimax.as_series())

59

60 # Print summary.

61 print("\nSummary:")

62 print(sarimax.as_summary())

63

64 # -----------------

65 # Save & Load

66 # -----------------

67 # File location

68 # fname = '../../examples/saved/arima-sample.pickle'

69

70 # Save

71 # arima.save(fname=fname)

72

73 # Load

74 # arima = ARIMAWrapper().load(fname=fname)

75

76

77 # -----------------

78 # Predict and plot

79 # -----------------

80 # This example shows how to make predictions using the wrapper which has

81 # been previously fitted. It also demonstrateds how to plot the resulting

82 # data for visualization purposes. It shows two different types of

83 # predictions:

84 # - dynamic predictions in which the prediction is done based on the

85 # previously predicted values. Note that for the case of ARIMA(0,1,1)

86 # it returns a line.

87 # - not dynamic in which the prediction is done based on the real

88 # values of the time series, no matter what the prediction was for

89 # those values.

90

91 # Variables.

92 s, e = 50, 120

93

94 # Compute predictions

95 preds_1 = sarimax.get_prediction(start=s, end=e, dynamic=False)

96 preds_2 = sarimax.get_prediction(start=s, end=e, dynamic=True)

97

98 # Create figure

99 fig, axes = plt.subplots(1, 2, figsize=(8, 3))

100

101 # ----------------

102 # Plot non-dynamic

103 # ----------------

104 # Plot truth values.

105 axes[0].plot(y, color='#A6CEE3', alpha=0.5, marker='o',

106 markeredgecolor='k', markeredgewidth=0.5,

107 markersize=5, linewidth=0.75, label='Observed')

108

109 # Plot forecasted values.

110 axes[0].plot(preds_1[0, :], preds_1[1, :], color='#FF0000', alpha=1.00,

111 linewidth=2.0, label=sarimax._identifier())

112

113 # Plot the confidence intervals.

114 axes[0].fill_between(preds_1[0, :], preds_1[2, :],

115 preds_1[3, :],

116 color='#FF0000',

117 alpha=0.25)

118

119 # ------------

120 # Plot dynamic

121 # ------------

122 # Plot truth values.

123 axes[1].plot(y, color='#A6CEE3', alpha=0.5, marker='o',

124 markeredgecolor='k', markeredgewidth=0.5,

125 markersize=5, linewidth=0.75, label='Observed')

126

127 # Plot forecasted values.

128 axes[1].plot(preds_2[0, :], preds_2[1, :], color='#FF0000', alpha=1.00,

129 linewidth=2.0, label=sarimax._identifier())

130

131 # Plot the confidence intervals.

132 axes[1].fill_between(preds_2[0, :], preds_2[2, :],

133 preds_2[3, :],

134 color='#FF0000',

135 alpha=0.25)

136

137 # Configure axes

138 axes[0].set_title("ARIMA non-dynamic")

139 axes[1].set_title("ARIMA dynamic")

140

141 # Format axes

142 axes[0].grid(True, linestyle='--', linewidth=0.25)

143 axes[1].grid(True, linestyle='--', linewidth=0.25)

144

145 # Legend

146 axes[0].legend()

147 axes[1].legend()

148

149 # Show

150 plt.show()

Total running time of the script: ( 0 minutes 0.492 seconds)